Dr. Dinesh

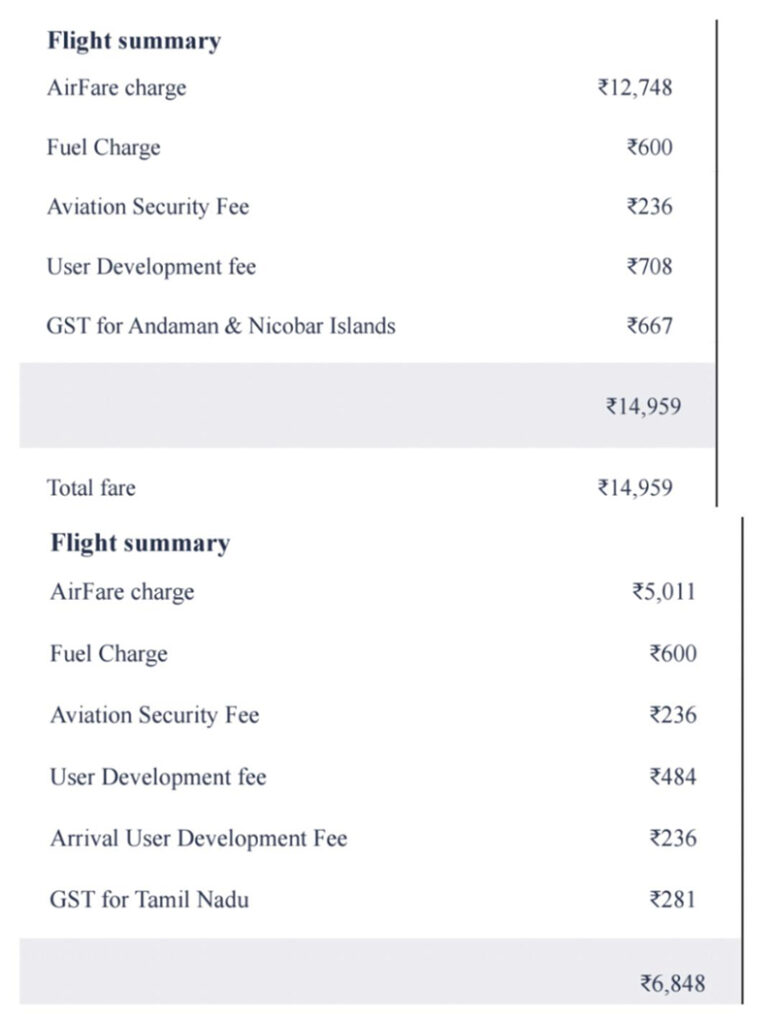

Air travel to island territories is not a luxury; it is a lifeline. For residents of the Andaman & Nicobar Islands, aviation remains the only dependable mode of connectivity for medical emergencies, higher education, trade, and administrative access. Yet, the structure of domestic airfares continues to burden passengers with layers of charges that often inflate the final ticket cost far beyond the base fare.

A typical one-way ticket includes fuel surcharge, aviation security fee, user development fee (departure), arrival user development fee, and Goods and Services Tax (GST), in addition to the basic airfare. While GST is a statutory levy and cannot be waived without a decision of the GST Council, most other components are administrative or regulatory charges. In principle, these can be reduced, subsidised, or temporarily waived through policy intervention.

The case for such relief in island sectors is compelling. Unlike mainland routes, where rail and road offer viable alternatives, island residents have no choice but to fly. High fares, therefore, cease to reflect market dynamics and instead become barriers to essential mobility. Waiving or subsidising non-tax components such as UDF, ASF, and fuel surcharge could significantly reduce ticket costs without distorting tax structures. Even partial rationalisation would offer immediate and meaningful relief.

There is precedent. The regional connectivity framework has demonstrated that targeted subsidies and capped fares can improve accessibility without undermining airline viability. A similar “island connectivity” model, retaining GST while waiving other charges, would strike a balance between fiscal prudence and social obligation. Such an approach could be jointly implemented by the Ministry of Civil Aviation, airport regulators, and airlines.

The broader question is one of equity. Remote Andaman Island should not bear disproportionately higher costs for basic connectivity. If air travel is to be treated as essential infrastructure for island regions, pricing mechanisms must reflect that reality. Rationalising non-tax levies is not merely a financial adjustment; it is a policy signal that connectivity to the islands is a national priority.

Reducing the burden of ancillary charges, while retaining GST as mandated, would be a pragmatic first step. For island communities, it would mean more than cheaper tickets, it would mean access, inclusion, and a reaffirmation that geography should not determine opportunity.